ECB quantitative easing so far successful?

As the latest discussion of monetary policy numbers here has shown, the monetary policy of the European Central Bank (ECB) has not been expansionary since the beginning of the Great Recession in the year 2008. In March 2015 however, the ECB has started a „quantative easing“ (QE) program following the policy of the US central bank (Fed), which started its QE-program in November 2008. Meanwhile the ECB has bought government bonds worth more than 300 billion Euro. Thus the question arises, whether the QE-program has been successful so far in steering the inflation rate closer to the 2% target? According to the latest press statement of ECB chief economist Peter Praet, it has. The following analysis of monetary policy numbers casts however serious doubts on this optimistic assessment.

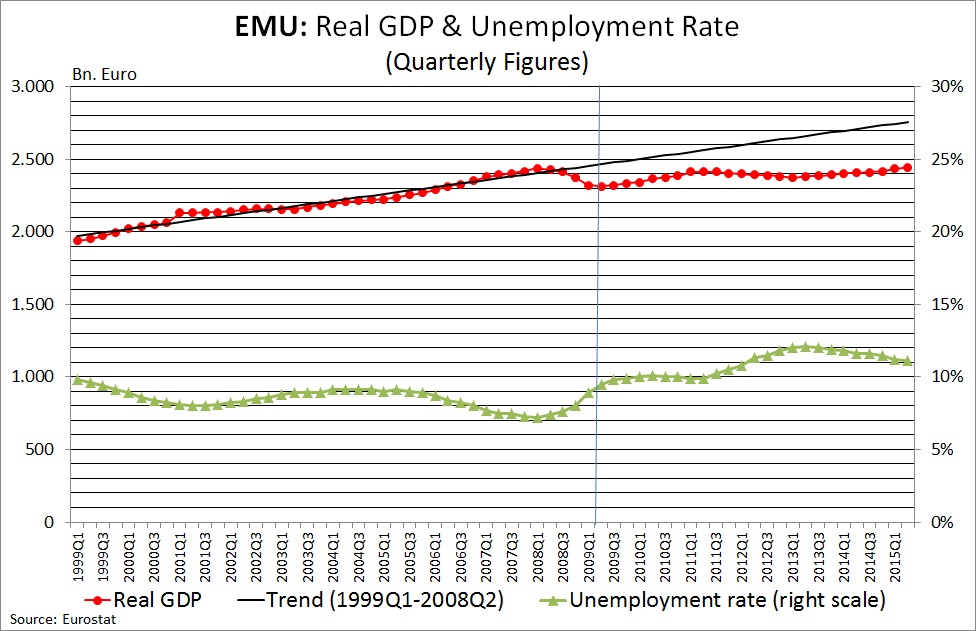

Figure 1 – Development of real GDP and unemployment EMU vs. USA

– Click diagrams to enlarge –

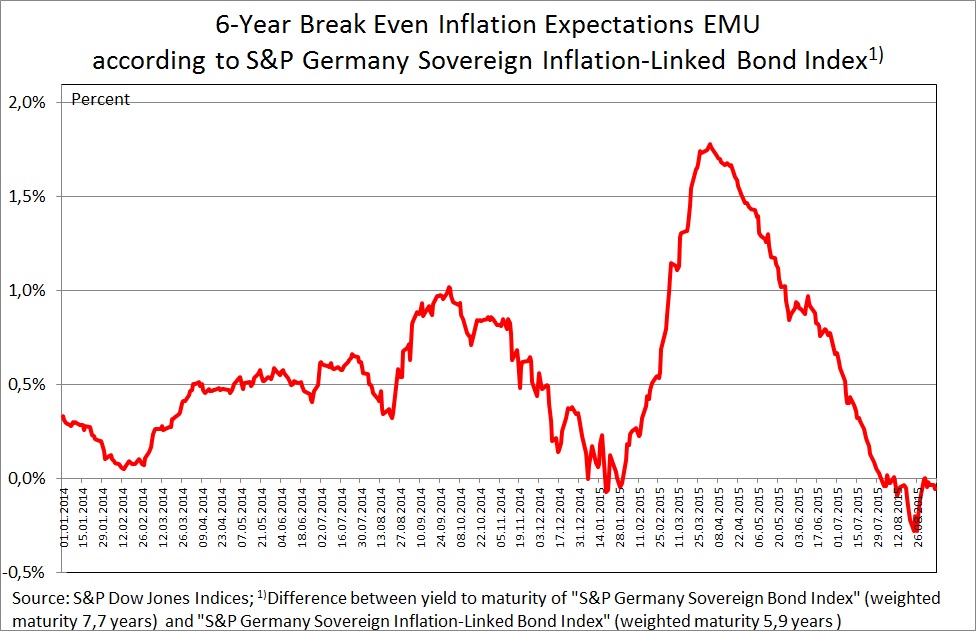

Market inflation expectations back to zero

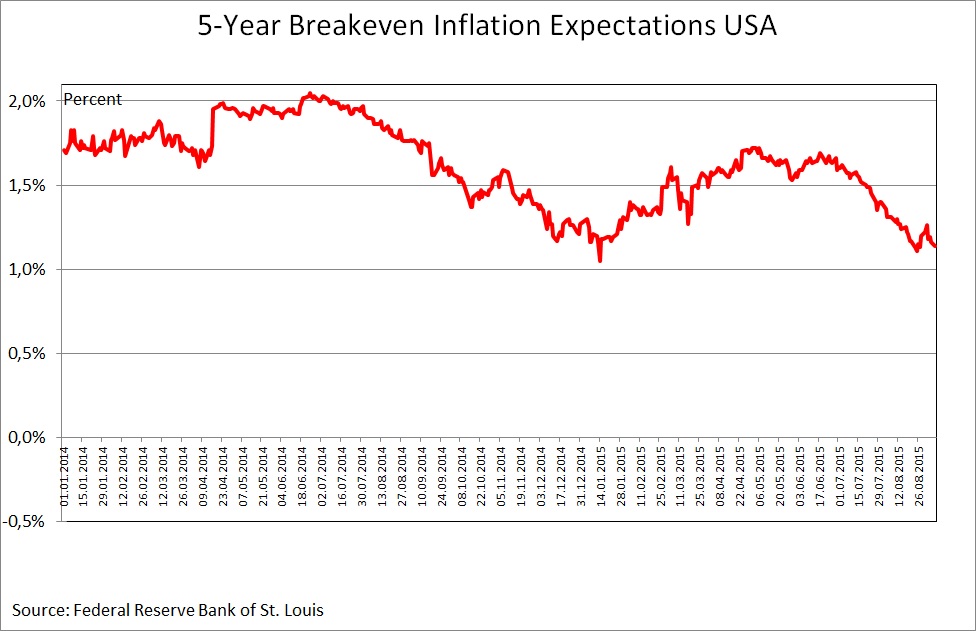

No doubt, the ECB QE-program had started extremly promising. By the end of January, shortly after it was anounced and before any asset had been bought, market inflation expectations started to rise. Super Mario seemed to be back! Figure 2 measures market inflation expectations by the difference of the interest rate of a nominal bond, it,t+n, and the real interest rate of an indexed bond, rt,t+n. Assuming that the theory behind the „expectation augmented Fisher equation“ works, the difference should equal the expected inflation rate, Et(πt,t+n), plus the risk premium, pt,t+n, for holding a nominal (=not inflation-protected) bond: Et(πt,t+n) + pt,t+n = it,t+n – rt,t+n. Unfortunately and contrary to the Fed, the ECB does not publish representative numbers for inflation-indexed bonds and does not plan to do so, according to an information from the ECB Statistics Hotline. The estimation presented in figure 2 is therefore based on data of the „S&P Germany Sovereign Bond Index“ (with an average maturity of 5,9 years) and the „S&P Germany Sovereign Inflation-Linked Bond Index“ (with an average maturity of 7,7 years). Even though the maturities do not exactly fit, the very strong increase of estimated market inflation expectations after the ECB QE-program was anounced, as well as the fall-back three weeks after the ECB started to buy bonds, should hardly be caused by an estimation error. And since the breakeven inflation rates implied by US-government bonds did not fall back to the same degree, it is not very likely that the fall-back of EMU market inflation expectations was caused by factors like an expected fall in oil prices.

Figure 2 – Market Inflation Expectations EMU vs. USA

– Click diagrams to enlarge –

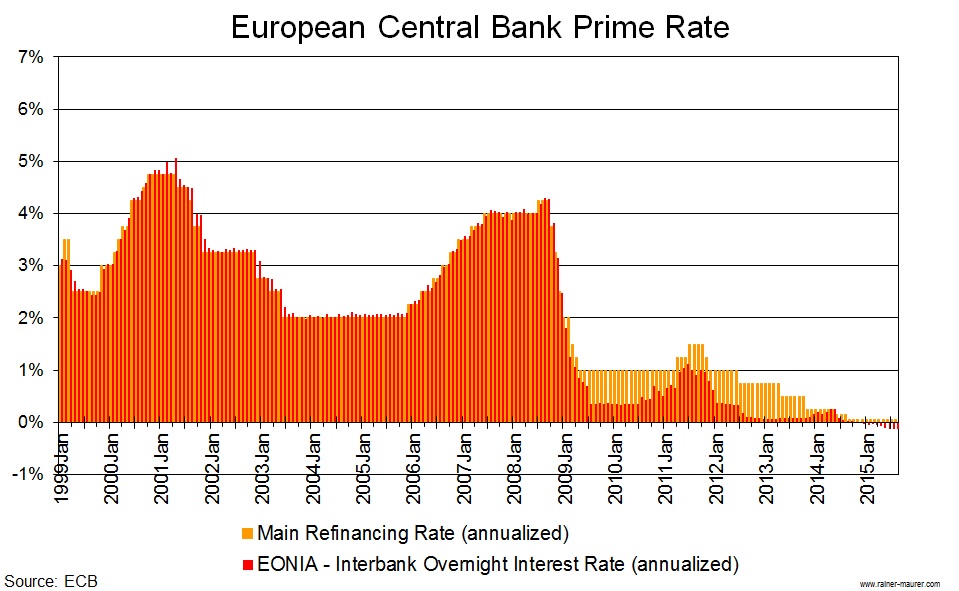

Failing credit growth

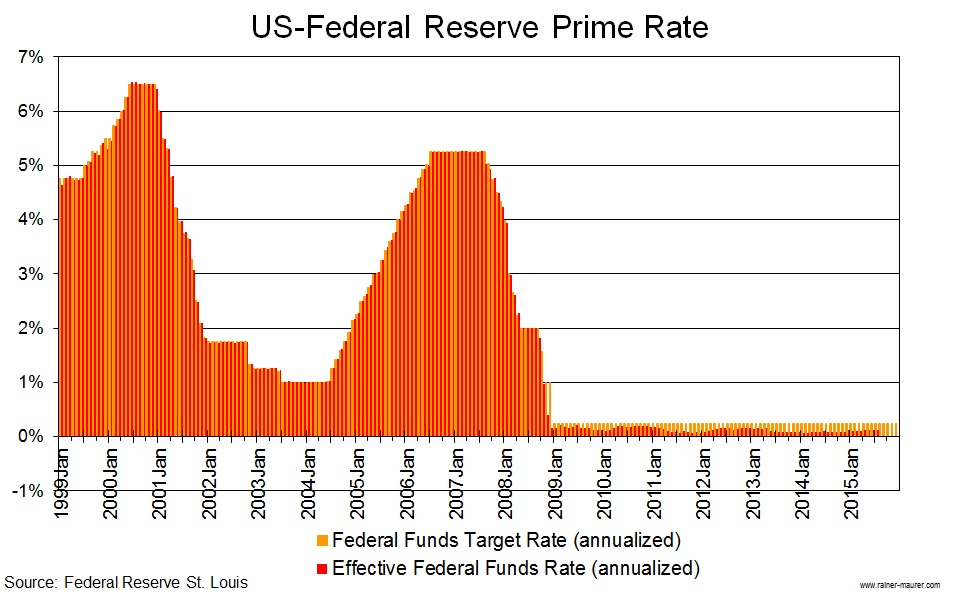

Why did inflation expectations fall back so shortly after the ECB QE-program started? A simple answer supported by the following data is, markets became aware that it does not work: Even though EMU interest rates have come remarkably down, credit growth is failing. Figure 3 shows that the EMU interbank interest rate with the shortest maturity (EONIA) has become negative – following the ECB deposit facility rate, which equals -0,20%.

Figure 3 – Prime Rates EMU vs. USA

– Click diagrams to enlarge –

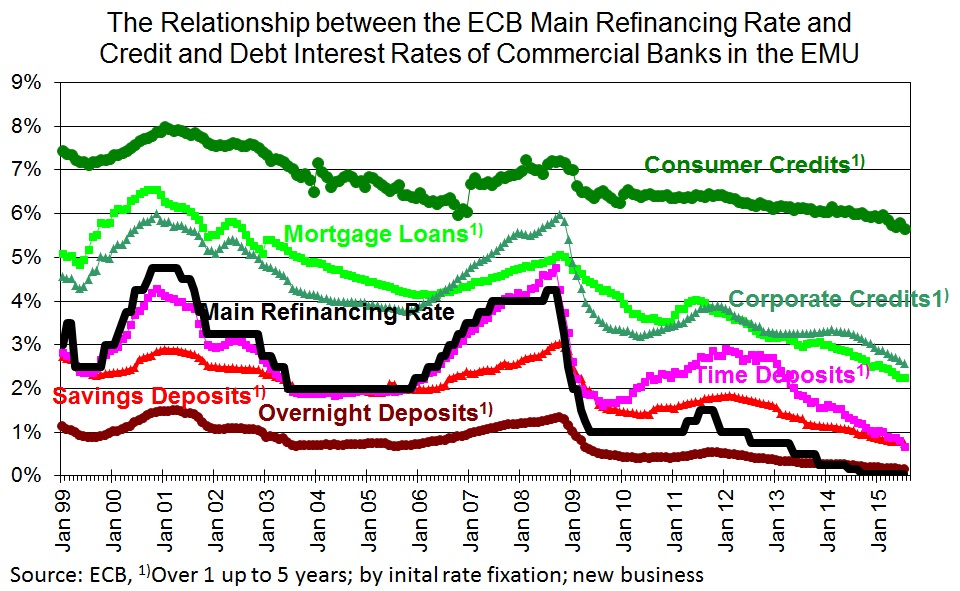

Figure 4 shows that the average interest rates for consumer credits, mortgage loans and corporate credits have followed the strong downward move of the ECB main refinancing rate. In fact the positive correlation between the main refinancing rate and credit interest rates, as measured by the correlation coefficient, has become even stronger after the decrease of the main refinancing rate at the beginning of the year 2009. The problem is however, that total lending of commercial banks to the private sector is still far away from the levels before the crisis (right-hand diagram of figure 4) and still displays no clear upward trend.

Figure 4 – Commercial Bank Interests Rates and Change of Total Credit Supply

– Click diagrams to enlarge –

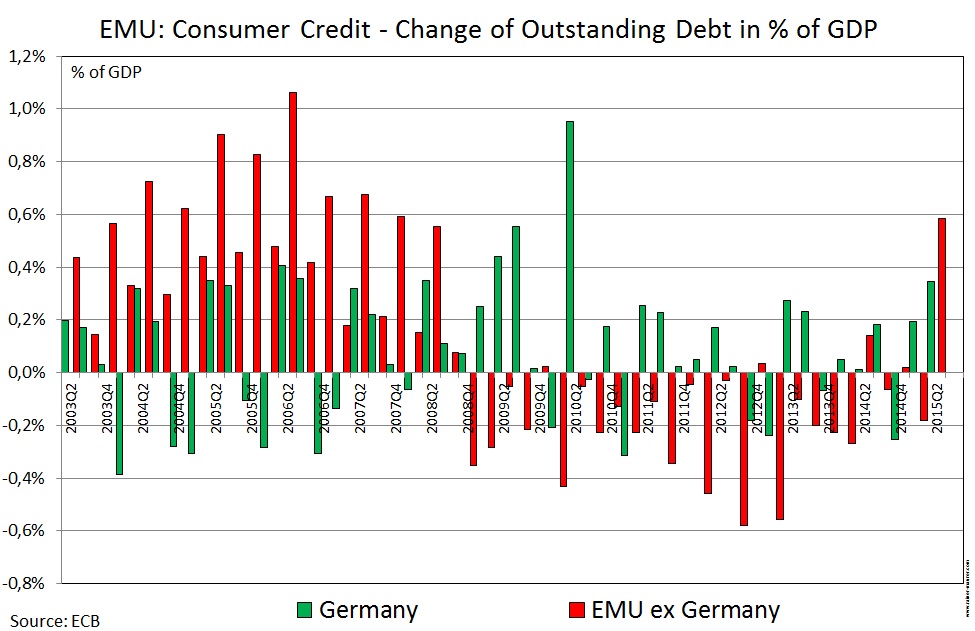

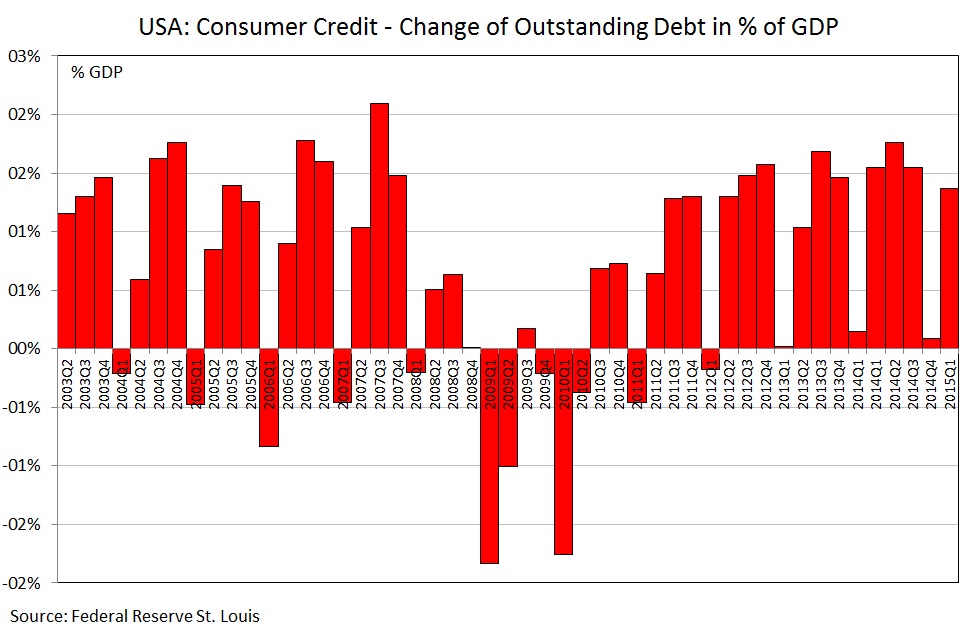

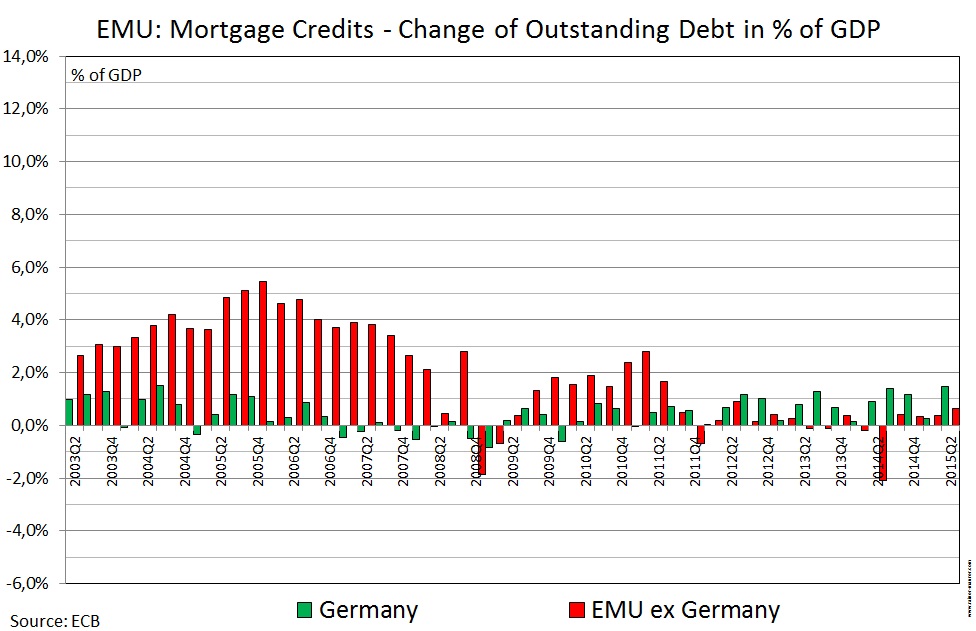

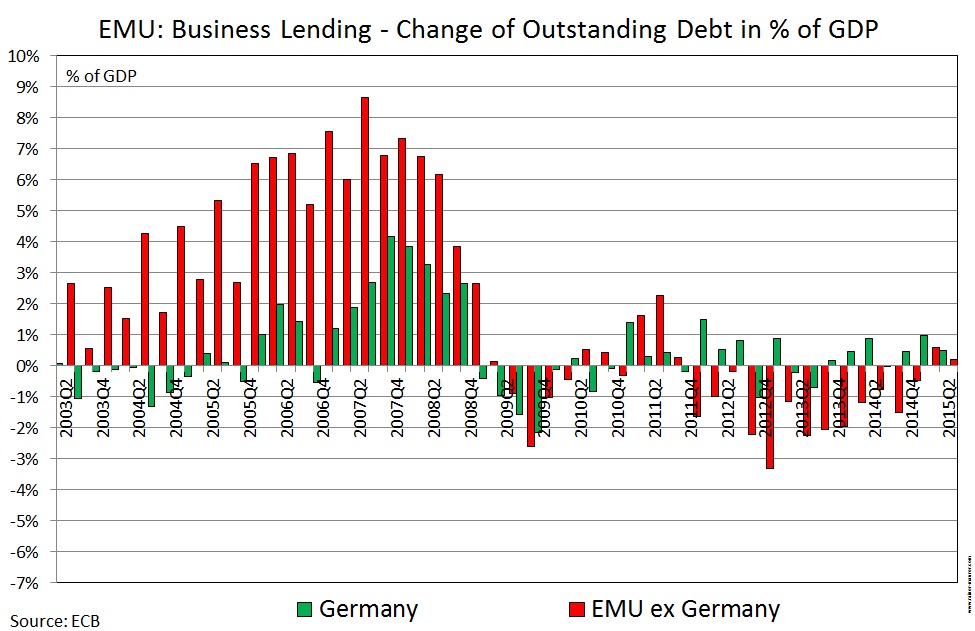

On a disaggregated level, only consumer credit growth seems to display a kind of recovery for Germany and the other EMU member states, while mortgage credit growth is back to pre-crisis levels only for Germany and business lending, the most important credit market segment in the EMU, is still significantly below pre-crisis levels – even for Germany (figure 5).

Figure 5 – Credit Growth EMU vs. USA

– Click diagrams to enlarge –

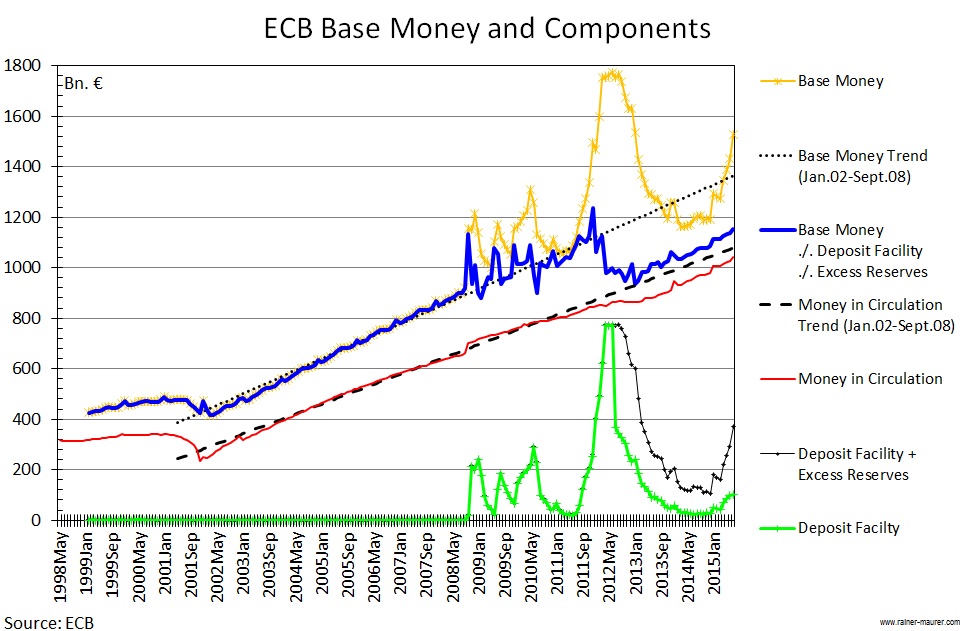

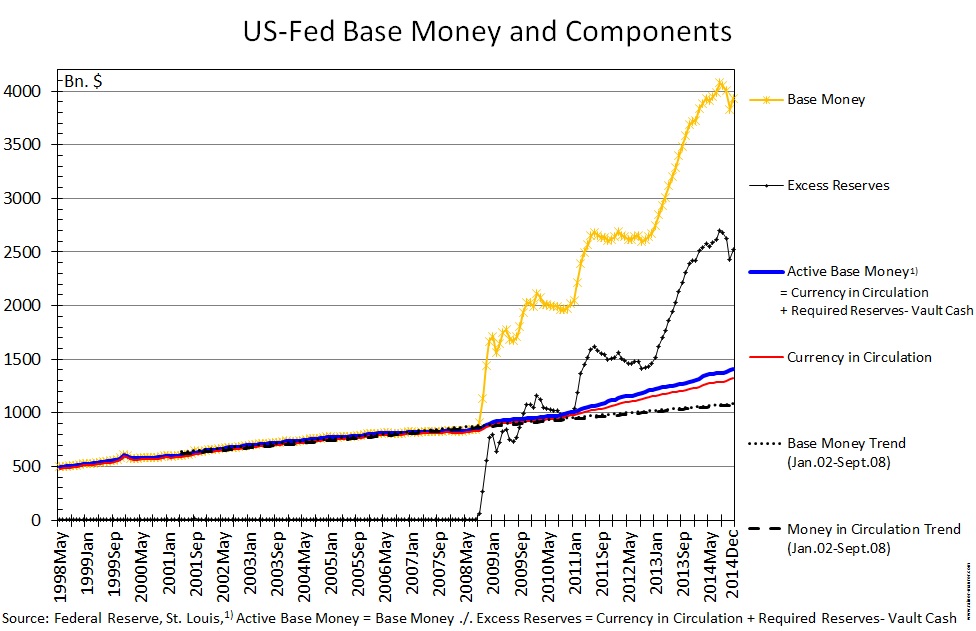

The ECB QE-program ends up in growing excess reserves

So, if the additional money supplied by the ECB QE-program does not cause an increase of credit growth, where is all the QE-money going? Figure 6 shows that most of this money ends up in the deposit facility and excess reserves held by commercial banks at their ECB-accounts – even though for both accounts the same negative interest rate of -0,20% is paid. In other words, the money does not actually leave the ECB. As a result, active base money (= currency in circulation plus the required minimum reserves = base money minus deposit facility minus excess reserves) is still far below its long-run trend level, indicating that the monetary policy of the ECB is still not expansionary – at least by good old monetarist standards. This leads to the question, why do commerical banks sell government bonds, which pay a positive nominal interest rate, to the ECB and keep the largest part of the revenues on ECB accounts, which pay a negative interest rate? Whatever the true answer is, the EMU commerical banking sector seems to be far away from a normalization of business.

Figure 6 – Base Money and Components EMU vs. USA

– Click diagrams to enlarge –

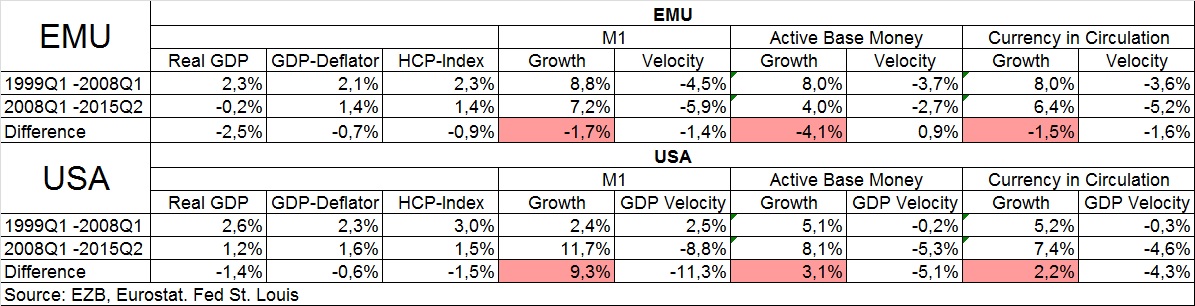

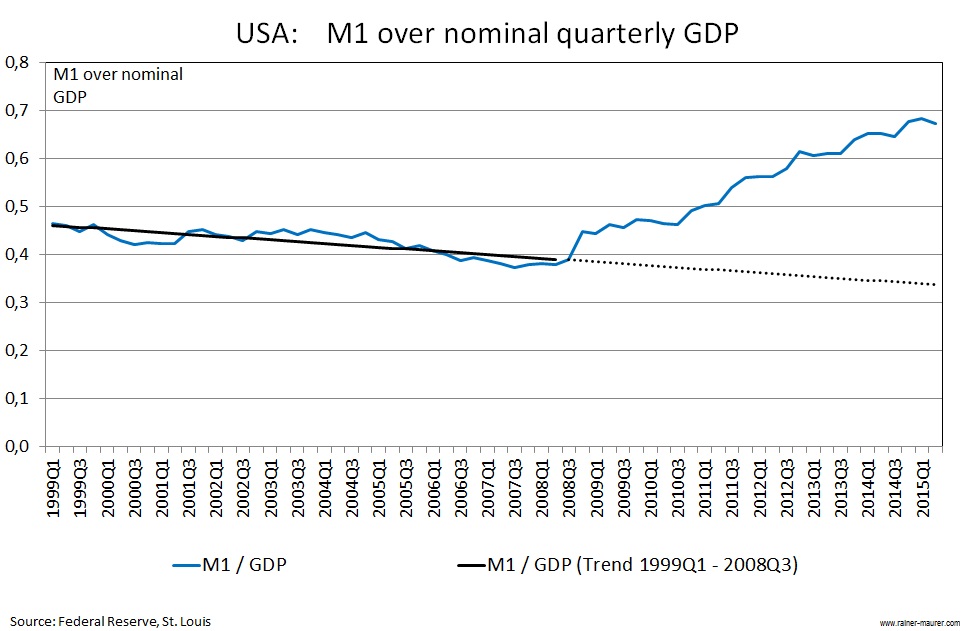

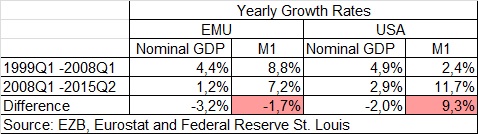

As the update of the remaining diagrams show, the relation between monetary aggregates over nominal GDP is not improving either in comparison to the last analysis here – with exception of M1 over nominal GDP, which displays now a slight upward trend – due to a downward revision of nominal GDP data.

Figure 7 – Monetary Aggregates over nominal GDP EMU vs. USA

– Click diagrams to enlarge –